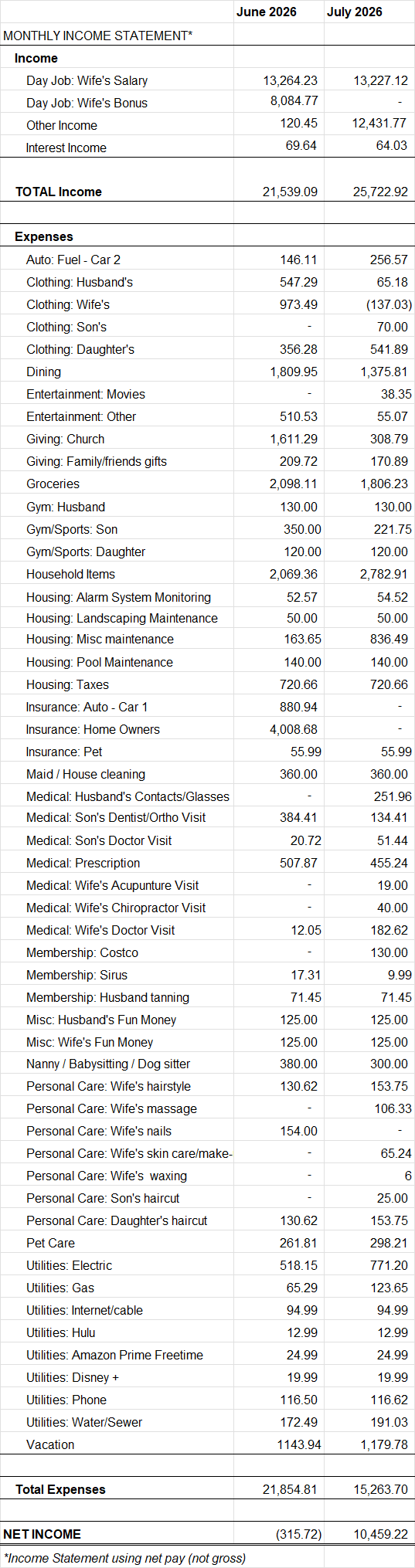

In July, we had an incredible income month and a reasonable expense month by comparison.

This month, our total net income was $25,722.92. In addition to my wife’s regular paychecks, we sold $12,109.75 worth of stock and received $134.98 in company reimbursements. She also unexpectedly received $187.04 from class action lawsuit. We earned $64.03 in interest income from our savings account.

Our expenses this month totaled $15,263.70. Large, non-fixed expenses included $1, 179.78 for vacation, $1, 134.67 for medical/dental/prescriptions, and $510.07 in personal care.

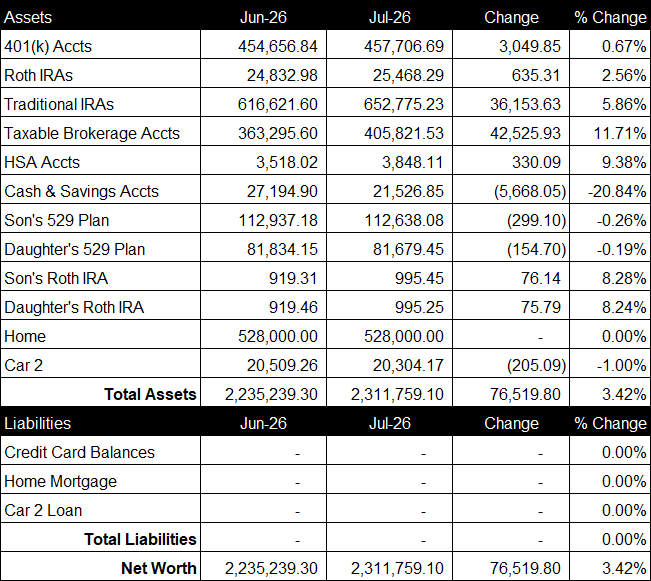

July was good month for our net worth. Our net worth increased $76,519.80 from last month to a total of $2,311,759.80 (see spreadsheet screenshot).

Retirement Accounts

Our retirement accounts are comprised of our 401(k)s, our Roth IRAs and our Traditional IRAs. My Wife contributes 8% to her 401(k) and her company matches 4% and chips in an additional 6% (lump sum) every March. Her 401(k) contribution increases by 1% automatically in March. This month, she contributed $1,523.04 to her 401(k). I do not work and do not contribute to a retirement account any longer. The total balance of our retirement accounts increased $39,838.79 from last month to a total of $1,135,950.21.

HSA Account

We plan to pull from this bucket for health related expenses once my Wife retires. Her company contributes $2,000 annually and we contribute $125 each paycheck. The total current value of the HSA accounts is $3,848.11.

Brokerage Account

Currently, our brokerage accounts consist of stocks and cryptocurrency (I prefer to track crypto in the “Brokerage Accounts” field rather than “Cash & Savings Accounts”). The total current value of our brokerage accounts is $405,821.53, up $42,525.93 from last month.

Cash & Savings Account

Cash and savings accounts consist of a small sum of cash at home, our online savings accounts balance. It does not include our checking account balance that we use to pay our bills each month. Our savings decreased $5,668.05 this month to a total of $21,562.85.

College Savings Accounts

This month, we contributed $232 to our son’s 529 Plan and it decreased $299.10 from last month to

a total balance of $112,638.08. We contributed $232 to our daughter’s 529 Plan and it decreased $154.70 from last month to a total balance of $81,679.45. Our total 2026 contributions so far are $3,596 for our son and $3,596 for our daughter (2026 goal is $4,750 in contributions for each child).

Children’s Roth IRAs

This month, we contributed $0 to our son’s Roth IRA and it increased $76.14, to $995.45. We contributed $0 to our daughter’s Roth IRA and it increased $76.79, to $995.25. We will be the custodian until our kids turn 18 years old, then the accounts will be transferred into their names.

Home

For our home value, we use the $528K purchase price that we paid in July 2016. Current comps in the area are ~$912K. We paid off our home in September 2021.

Vehicles

My wife drives a company vehicle and has a company gas card. I drive a 2017 SUV (~117K miles on odometer) that we own (no auto loan). My wife gets a new company car next month and it’s a nice one (she receives a better selection of vehicles after her promotion).

Credit Card Balance

All of our credit card debt is paid in full each month.

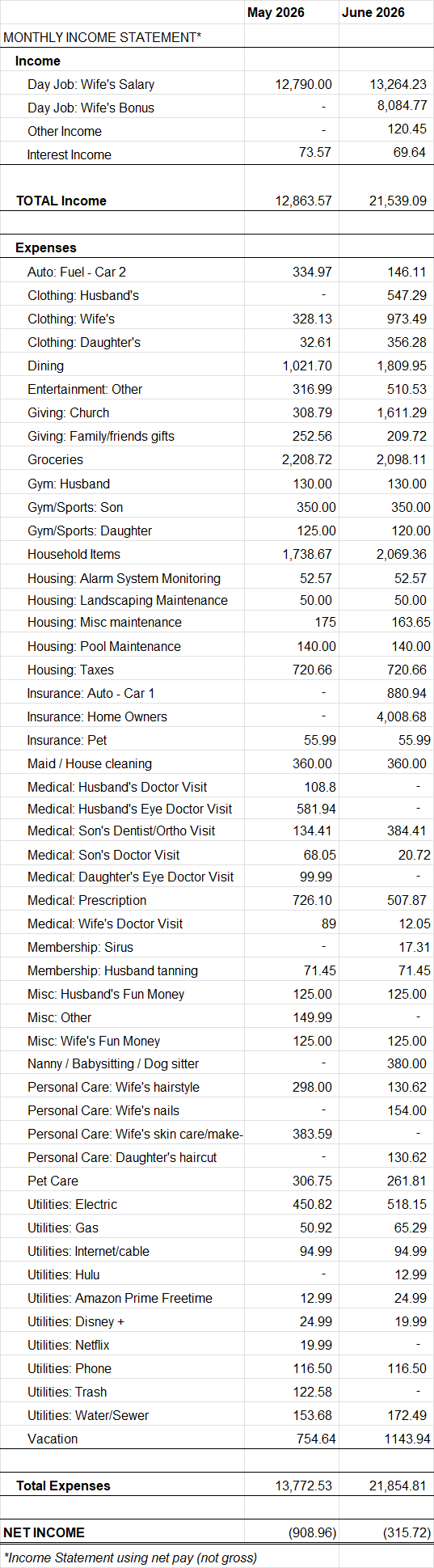

In June, we had both a high income month and a high expense month.

This month, our total net income was $21,539.09. In addition to my wife’s regular paychecks, she received a quarterly bonus of $13,025 gross ($8,084.77 net) and $120.45 in company reimbursements. We also earned $69.64 in interest income from our savings account.

Our expenses this month totaled $21,854.81. Large, non-fixed expenses included $1,143.94 for vacation, $1,877.06 for clothing, and $925.05 for medical/dental/prescriptions.

Next month, my wife should be able to sell some company stock.

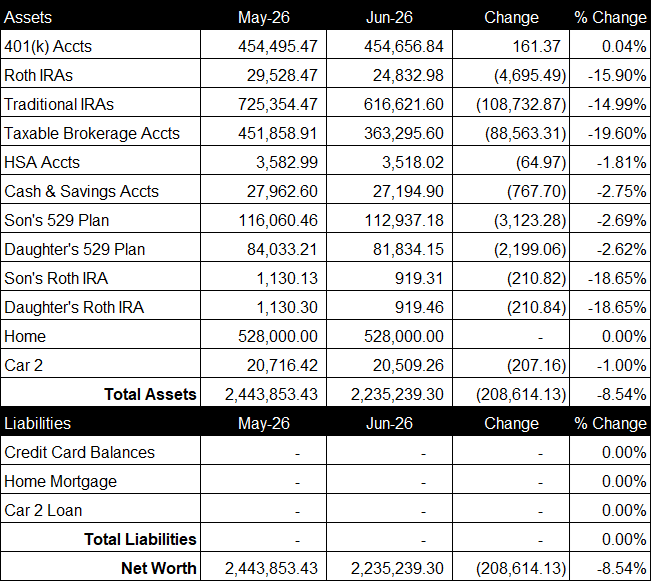

June was brutal month for our net worth. Our net worth decreased $208,614.13 from last month to a total of $2,235,239.30 (see spreadsheet screenshot).

Retirement Accounts

Our retirement accounts are comprised of our 401(k)s, our Roth IRAs and our Traditional IRAs. My Wife contributes 8% to her 401(k) and her company matches 4% and chips in an additional 6% (lump sum) every March. Her 401(k) contribution increases by 1% automatically in March. This month, she contributed $2,174.29 to her 401(k). I do not work and do not contribute to a retirement account any longer. The total balance of our retirement accounts decreased $113,266.99 from last month to a total of $1,096, 111.42.

HSA Account

We plan to pull from this bucket for health related expenses once my Wife retires. Her company contributes $2,000 annually and we contribute $125 each paycheck. The total current value of the HSA accounts is $3,518.02.

Brokerage Account

Currently, our brokerage accounts consist of stocks and cryptocurrency (I prefer to track crypto in the “Brokerage Accounts” field rather than “Cash & Savings Accounts”). The total current value of our brokerage accounts is $363,295.60, down $88,563.31 from last month.

Cash & Savings Account

Cash and savings accounts consist of a small sum of cash at home, our online savings accounts balance. It does not include our checking account balance that we use to pay our bills each month. Our savings decreased $767.70 this month to a total of $27,194.90.

College Savings Accounts

This month, we contributed $232 to our son’s 529 Plan and it decreased $3,123 from last month to a total balance of $112,937.18. We contributed $232 to our daughter’s 529 Plan and it decreased $2,199.06 from last month to a total balance of $81,834.15. Our total 2026 contributions so far are $3,364 for our son and $3,364 for our daughter (2026 goal is $4,750 in contributions for each child).

Children’s Roth IRAs

This month, we contributed $0 to our son’s Roth IRA and it decreased $210.82, to $919.31. We contributed $0 to our daughter’s Roth IRA and it decreased $210.84, to $919.46. We will be the custodian until our kids turn 18 years old, then the accounts will be transferred into their names.

Home

For our home value, we use the $528K purchase price that we paid in July 2016. Current comps in the area are ~$931K. We paid off our home in September 2021.

Vehicles

My wife drives a company vehicle and has a company gas card. I drive a 2017 SUV (~115K miles on odometer) that we own (no auto loan). My wife gets a new company car next month and it’s a nice one (she receives a better selection of vehicles after her promotion).

Credit Card Balance

All of our credit card debt is paid in full each month.

In May, we had a pretty typical income month and expense month.

This month, our total net income was $12,863.57. In addition to my wife’s regular paychecks, we earned $73.57 in interest income from our savings account.

Our expenses this month totaled $13,772.53. Large, non-fixed expenses included $1,808.29 for medical/dental/prescriptions, $754.64 for vacation, $681.59 for personal care items.

Next month, my wife should receive a quarterly bonus of 13,025 gross.

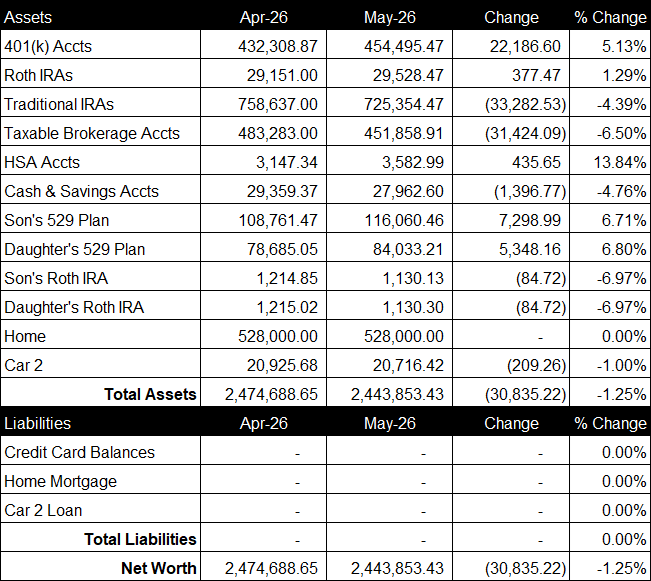

May looked promising but ended as a down month our net worth. Our net worth decreased $30,835.22 from last month to a total of $2,443,853.43 (see spreadsheet screenshot).

Retirement Accounts

Our retirement accounts are comprised of our 401(k)s, our Roth IRAs and our Traditional IRAs. My Wife contributes 8% to her 401(k) and her company matches 4% and chips in an additional 6% (lump sum) every March. Her 401(k) contribution increases by 1% automatically in March. This month, she contributed $1,523.04 to her 401(k). I do not work and do not contribute to a retirement account any longer. The total balance of our retirement accounts decreased $10,718.46 from last month to a total of $1,209,378.41.

HSA Account

We plan to pull from this bucket for health related expenses once my Wife retires. Her company contributes $2,000 annually and we contribute $125 each paycheck. The total current value of the HSA accounts is $3, 582.99

Brokerage Account

Currently, our brokerage accounts consist of stocks and cryptocurrency (I prefer to track crypto in the “Brokerage Accounts” field rather than “Cash & Savings Accounts”). The total current value of our brokerage accounts is $451,858.91, down $31,424.09 from last month.

Cash & Savings Account

Cash and savings accounts consist of a small sum of cash at home, our online savings accounts balance. It does not include our checking account balance that we use to pay our bills each month. Our savings decreased $1,396.77 this month to a total of $27,962.60.

College Savings Accounts

This month, we contributed $232 to our son’s 529 Plan and it increased $7,298.99 from last month to a total balance of $116,060.46. We contributed $232 to our daughter’s 529 Plan and it increased $5,348.16 from last month to a total balance of $84,033.21. Our total 2026 contributions so far are $3,132 for our son and $3,132 for our daughter (2026 goal is $4,750 in contributions for each child).

Children’s Roth IRAs

This month, we contributed $0 to our son’s Roth IRA and it decreased $84.72, to $1,130. 13. We contributed $0 to our daughter’s Roth IRA and it decreased $84.72, to $1,130.30. We will be the custodian until our kids turn 18 years old, then the accounts will be transferred into their names.

Home

For our home value, we use the $528K purchase price that we paid in July 2016. Current comps in the area are ~$931K. We paid off our home in September 2021.

Vehicles

My wife drives a company vehicle and has a company gas card. I drive a 2017 SUV (~115K miles on odometer) that we own (no auto loan). My wife gets a new company car next month and it’s a nice one (she receives a better selection of vehicles after her promotion).

Credit Card Balance

All of our credit card debt is paid in full each month.

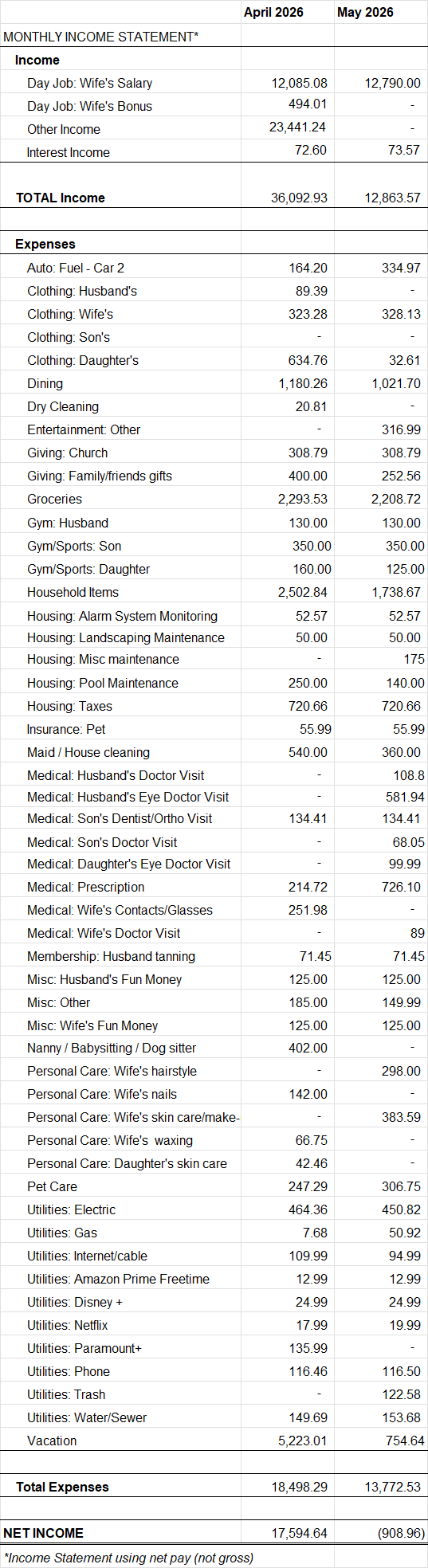

In April, we had another amazing income month and a reasonable expense month.

This month, our total net income was $36,092.93. In addition to my wife’s regular paychecks, she sold $22,101.87 of her company stock. She received $120 in company reimbursements this month, we received a $725.36 refund from Southwest Airlines, and we earned $72.60 in interest income from our savings account.

Our expenses this month totaled $17,594.64. Large, non-fixed expenses included $5223.01 for vacation, $1,047.43 for clothing, and $601.11 for medical expenses.

Next month, my wife’s paychecks will be larger because no social security will be deducted (hit max for year). This will be the case for the remainder of 2026 and should allow us to invest/save more money each month.

April was an incredible month our net worth. Our net worth increased $225,869.36 from last month to a total of $2,474,688.65 (see spreadsheet screenshot).

Retirement Accounts

Our retirement accounts are comprised of our 401(k)s, our Roth IRAs and our Traditional IRAs. My Wife contributes 8% to her 401(k) and her company matches 4% and chips in an additional 6% (lump sum) every March. Her 401(k) contribution increases by 1% automatically in March. This month, she contributed $1,523.04 to her 401(k). I do not work and do not contribute to a retirement account any longer. The total balance of our retirement accounts increased $131,296.41 from last month to a total of $1,220,096.87.

HSA Account

This is a new addition to our net worth tracking. We plan to pull from this bucket for health related expenses once my Wife retires. Her company contributes $2,000 annually and we contribute $125 each paycheck. The total current value of the HSA accounts is $3, 147.34.

Brokerage Account

Currently, our brokerage accounts consist of stocks and cryptocurrency (I prefer to track crypto in the “Brokerage Accounts” field rather than “Cash & Savings Accounts”). The total current value of our brokerage accounts is $483,283.00 up $70,254.53 from last month.

Cash & Savings Account

Cash and savings accounts consist of a small sum of cash at home, our online savings accounts balance. It does not include our checking account balance that we use to pay our bills each month. Our savings increased $4,096.19 this month to a total of $29,059.37.

College Savings Accounts

Our kids have 529 Plans through Vanguard. This month, we contributed $1,000 to our son’s 529 Plan and it increased $11,078.79 from last month to a total balance of $108,761.47. We contributed $1,000 to our daughter’s 529 Plan and it increased $8,545.07 from last month to a total balance of $78,685.05. Our total 2026 contributions so far are $2,900 for our son and $2,900 for our daughter (2026 goal is $4,750 in contributions for each child).

Children’s Roth IRAs

We just opened Roth IRAs through Fidelity for our two kids. This month, we contributed $0 to our son’s Roth IRA and it increased to $1,214.85. We contributed $0 to our daughter’s Roth IRA and it increased to $1,215.02. We will be the custodian until our kids turn 18 years old, then the accounts will be transferred into their names.

Home

For our home value, we use the $528K purchase price that we paid in July 2016. Current comps in the area are ~$927K. We paid off our home in September 2021.

Vehicles

My wife drives a company vehicle and has a company gas card. I drive a 2017 SUV (~115K miles on odometer) that we own (no auto loan). My wife gets a new company car next month and it’s a nice one (she receives a better selection of vehicles after her promotion).

Credit Card Balance

All of our credit card debt is paid in full each month.

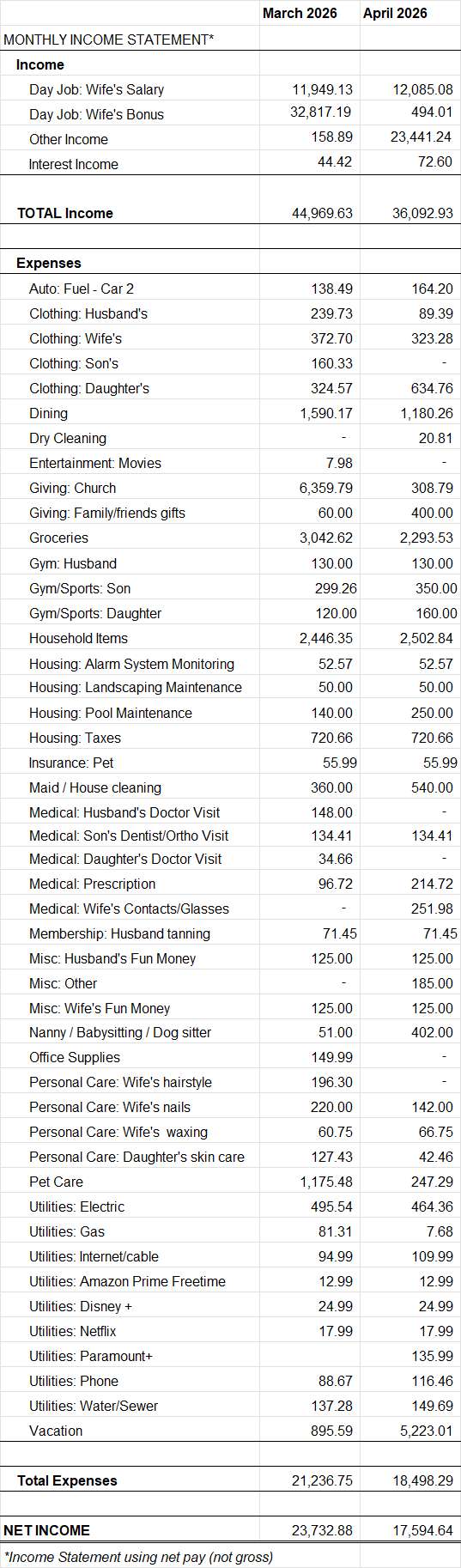

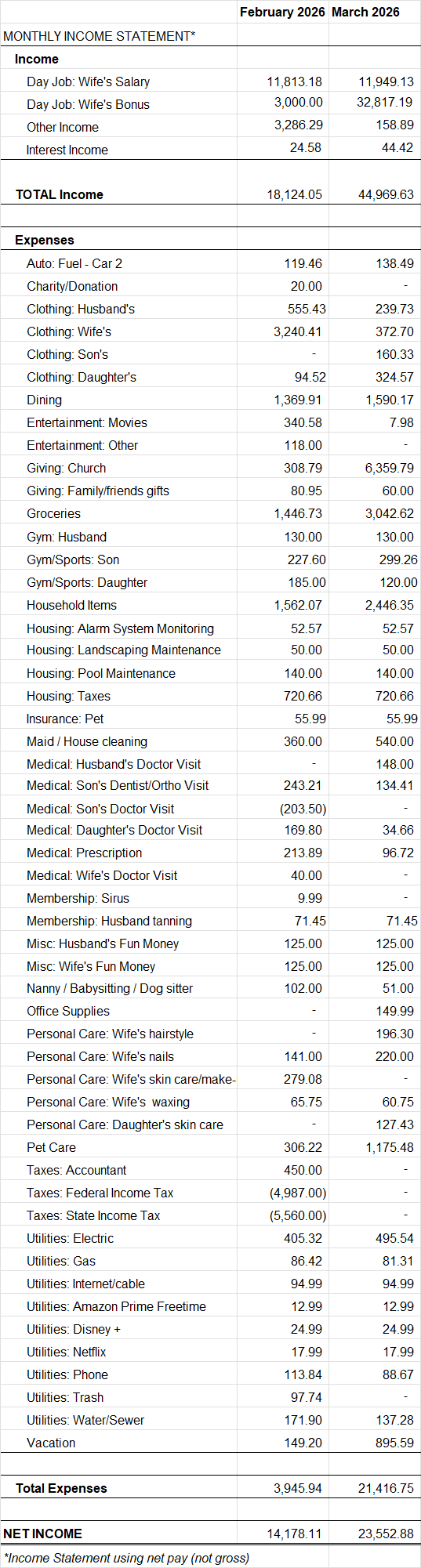

In March, we had an amazing income month and a high, but relatively reasonable expense month compared to income.

This month, our total net income was $44,969.63. My Wife’s 4% raise went into affect this month. In addition to my wife’s regular paychecks, she received an incredible quarterly bonus of $60,509.13 gross ($32,817.19 net). Her company reimbursements were $158.89 this month and we earned $44.42 in interest income from our savings account.

This month, our expenses totaled $23,552.88. Large, non-fixed expenses includes $1,175.48 for pet care (our dog got sick), $1,097.33 for clothing, and $895.59 for vacation expenses.

Next month, my wife plans to sell some company stock that has vested. She didn’t sell it this month because of the stock market decline.

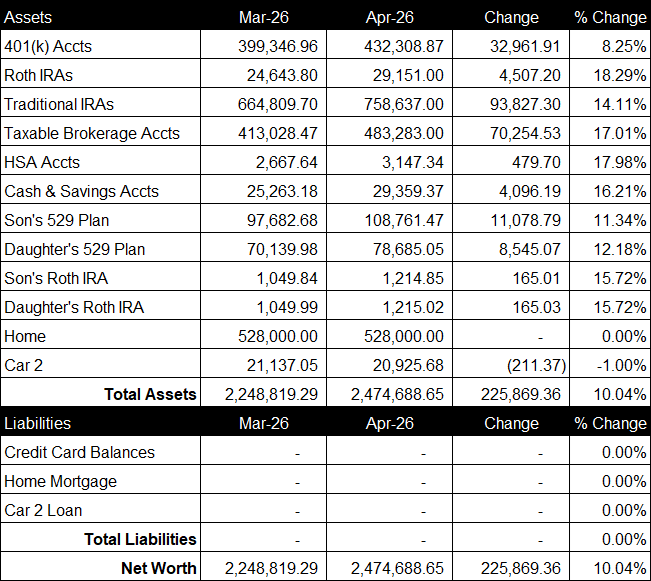

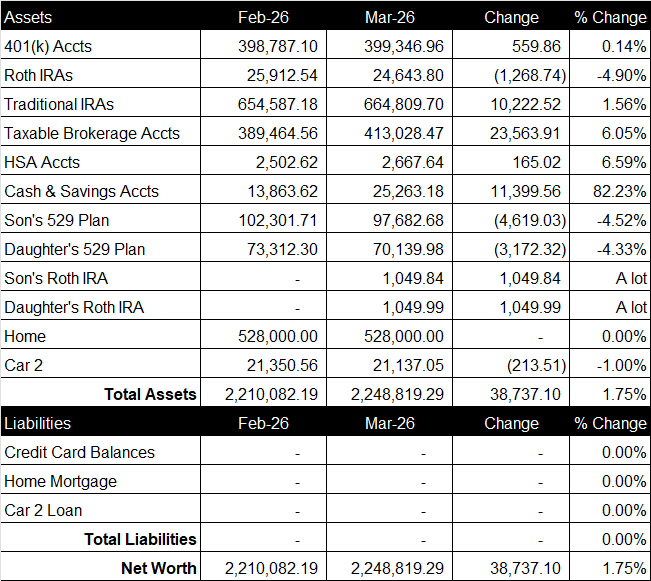

March was a positive month our net worth. Our net worth increased $38,737.10 from last month to a total of $2,248,819.29 (see spreadsheet screenshot).

Retirement Accounts

Our retirement accounts are comprised of our 401(k)s, our Roth IRAs and our Traditional IRAs. My Wife contributes 8% to her 401(k) and her company matches 4%, while also chipping in an additional 6% (lump sum) every March (the extra 6%, $19,014.22, was just deposited into her account). Her 401(k) contribution increases by 1% automatically in March every year (just increased from 7% to 8%). This month, she contributed $5119.64 to her 401(k). I do not work and do not contribute to a retirement account any longer. The total balance of our retirement accounts increased $9,513.64 from last month to a total of $1,088,800.46.

HSA Account

This is a new addition to our net worth tracking. We plan to pull from this bucket for health related expenses once my Wife retires. Her company contributes $2,000 annually and we contribute $125 each paycheck. The total current value of the HSA accounts is $2,667.64.

Brokerage Account

Currently, our brokerage accounts consist of stocks and cryptocurrency (I prefer to track crypto in the “Brokerage Accounts” field rather than “Cash & Savings Accounts”). The total current value of our brokerage accounts is $413,028.47 up $23,563.91 from last month.

Cash & Savings Account

Cash and savings accounts consist of a small sum of cash at home, our online savings accounts balance. It does not include our checking account balance that we use to pay our bills each month. Our savings increased $11,399.56 this month to a total of $25,263.18.

College Savings Accounts

Our kids have 529 Plans through Vanguard. This month, we contributed $500 to our son’s 529 Plan and it decreased $4,619.03 from last month to a total balance of $97,682.68. We contributed $500 to our daughter’s 529 Plan and it decreased $3,172.32 from last month to a total balance of $70,139.98. Our total 2026 contributions so far are $900 for our son and $900 for our daughter (2026 goal is $4,750 in contributions for each child).

Children’s Roth IRAs

We just opened Roth IRAs through Fidelity for our two kids. This month, we contributed $1,050 to our son’s Roth IRA and it decreased to $1,049.84. We contributed $1,050 to our daughter’s 529 Plan and it decreased to $1,049.99. We will be custodian until our kids turn 18 years old, then the accounts will be transferred into their names.

Home

For our home value, we use the $528K purchase price that we paid in July 2016. Current comps in the area are ~$922K. We paid off our home in September 2021.

Vehicles

My wife drives a company vehicle and has a company gas card. I drive a 2017 SUV (~115K miles on odometer) that we own (no auto loan). My wife gets a new company car next month and it’s a nice one (she receives a better selection of vehicles after her promotion).

Credit Card Balance

All of our credit card debt is paid in full each month.

Our path to financial independence and retiring early.